The Real Cost of SAF: Why the Unit Economics of Feedstock Will Decide Which Approach Replaces Fossil Fuels

When oil prices spike due to geopolitical events, no one is surprised to see jet fuel surcharges follow. This trend also leaves airline executives to once again face a familiar and stubborn challenge: depending on a single class of fuel, sourced through a handful of global chokepoints, is an existential business risk.

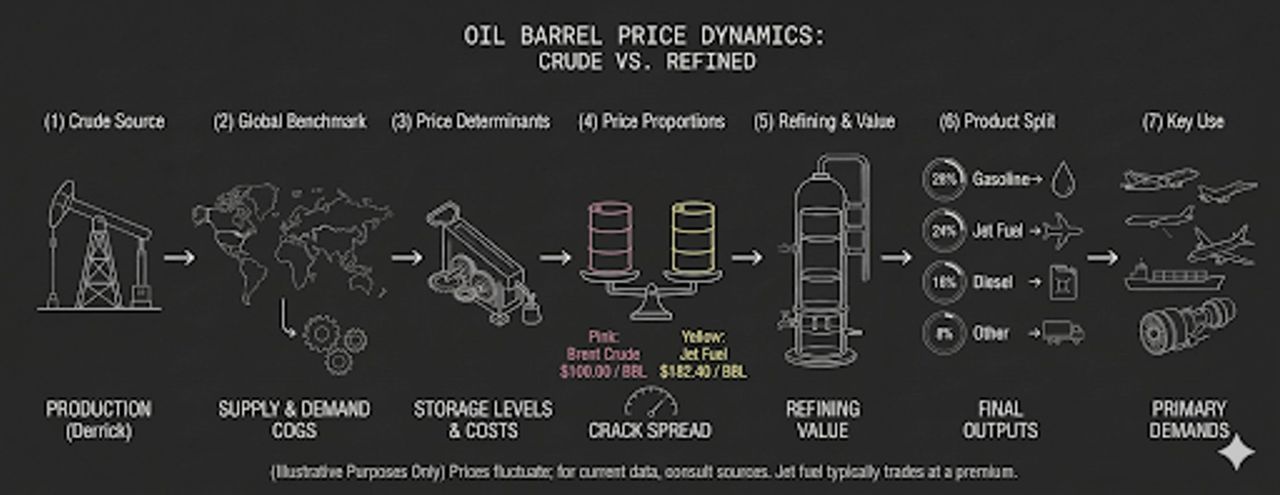

This schematic illustrates the journey from crude oil extraction to refined aviation fuel. It highlights the crack spread—the price gap between raw Brent crude (example price/barrel of $100.00) and finished jet fuel ($182.40) — visualized by proportional barrels and the distillation process required to meet primary global demands.

The sustainable aviation fuel (SAF) industry was supposed to offer a way out. To date, it has spent billions chasing better technology for converting raw materials into jet fuel. Despite this, the dominant SAF pathway today, derived from byproducts of the Hydroprocessed Esters and Fatty Acids (HEFA) process, relies on used cooking oil that is 80% sourced from China and shipped across the same trade lanes now under geopolitical stress. And the next generation of pathways depends on point-source CO₂ from industrial facilities tethered to expensive grid power.

Aviation doesn’t just need alternative fuel. It needs fuel built on feedstocks that are unlimited in supply and cannot be blockaded, embargoed, or priced out of reach by events half a world away. The reality is that most of today’s leading pathways are built on feedstocks that are either too scarce, too expensive, or too constrained by geography to reach the kind of scale that aviation demands.

Four Pathways. One Common Problem.

There are four fundamental routes to making synthetic jet fuel. Each one converts some combination of carbon and hydrogen into a liquid hydrocarbon. While the chemistry is well understood, the real challenge is sourcing millions of tons of those inputs, at the same location, at a cost that produces competitive fuel. Here’s where each pathway stands.

1. HEFA: Proven but Supply-Capped

HEFA is the most commercially mature SAF pathway. It upgrades biological oils, primarily used cooking oil (UCO) and crops like soy, into jet fuel by adding hydrogen. The technology is efficient and well-established, producing fuel at roughly $4 – $6 per gallon at the production level.

The problem is supply.

Over 80% of current SAF volumes depend on UCO, but global collection falls well short of demand. Europe alone consumes roughly eight times more UCO than it collects domestically, and the U.S. imported approximately 2.8 billion pounds from China in 2024 to bridge its own gap. Scaling HEFA to meet even a fraction of aviation’s fuel needs would require converting vast tracts of arable land to oil crop production, thereby competing directly with food supply. HEFA works today, but it has a hard ceiling.

2. Alcohol-to-Jet: Promising but Feedstock-Constrained

The alcohol-to-jet (ATJ) pathway converts ethanol into jet fuel. Facilities like LanzaJet’s Freedom Pines plant in Georgia are beginning to commercialize the process, with production costs estimated around $3 – $5 per gallon depending on the ethanol source.

The main issue here is where the ethanol comes from. Sugar-based ethanol, which is mostly derived from Brazilian sugarcane, faces the same food-versus-fuel constraint as HEFA. Cellulosic biomass (forest residue, corn stover, grasses) avoids that conflict but introduces a different bottleneck: it is extremely diffuse. Typical yields range from 1 – 6 dry tons per acre per year in many regions, and roughly ten tons of biomass are needed to produce one ton of fuel. At scale, the logistics of aggregating that material become prohibitively expensive.

3. Power-to-Liquid (RWGS): Right Idea, Wrong Economics

Reverse Water Gas Shift (RWGS) combines gaseous CO₂ with green hydrogen to produce syngas, then liquid fuel via Fischer-Tropsch synthesis. The chemistry is proven and widely viewed as one of the most promising long-term pathways. The feedstocks (just CO₂ and water) are abundant…in principle.

In practice, cost is the barrier. If CO₂ is captured from ambient air using today’s direct air capture (DAC) technology, it costs $600 – $1,000+ per metric ton. Green hydrogen adds another $4 – $6 per kilogram. With roughly four units of CO₂ needed per unit of fuel, feedstock costs alone push the price well above $10 per gallon.

Point-source capture from industrial emitters like cement or steel plants is cheaper, roughly $40 – $200 per ton. But this process introduces a location trap: co-locating a fuel plant at an industrial site means competing with the local grid for electricity, often at 2 – 3x the cost of renewables in remote, high-resource areas. You solve the CO₂ cost problem but inherit an energy cost problem.

4. CO₂ Electrolysis: Same Constraints

Direct CO₂ electrolysis faces an identical set of feedstock constraints as RWGS: it requires a pure stream of CO₂, green hydrogen, and co-located renewable energy. The binding constraint across both pathways is the same: getting cheap carbon, cheap hydrogen, and cheap electricity in one place. Our estimate is that these feedstock economics set a cost floor near $10 – $12 per gallon for any pathway relying on conventional DAC.

What Changes When Feedstock Comes from Air and Water

Sora was built to solve the feedstock problem directly. Our technology captures CO₂ from ambient air at below $50 per ton, which is a fraction of the $600 – $1,000+ that conventional DAC costs today. We achieve this through a novel liquid (bi)carbonate electrolyzer that integrates capture and conversion in a single closed-loop process, eliminating the energy-intensive regeneration step that dominates traditional DAC costs.

Critically, our system runs on intermittent renewable energy. That means we can locate production wherever solar or wind is cheapest. This typically means remote locations where power purchase agreements can run 60% below industrially available grid electricity, and where costs continue to fall. We don’t need to compete with data centers or industrial grids for power.

The result is a SAF pathway with only two feedstocks: air and water. They are ubiquitous, inexhaustible, and effectively free. When your carbon source costs under $50 per ton instead of $600 – $1,000, it doesn’t just improve unit economics, it changes the fundamental business model.

The Answer Is in the Air

The SAF industry has a technology surplus and a feedstock deficit. Every leading pathway – be it HEFA, alcohol-to-jet, RWGS, or CO₂ electrolysis – can convert carbon and hydrogen into jet fuel. The question is whether they can source those inputs at a cost and scale that makes the fuel competitive with fossil-derived jet fuel, which today averages around $2 – $3 per gallon wholesale.

The answer to that question for biological feedstocks,conventional DAC and point-source capture is a resounding “No.” The winners in SAF will be those who solve the feedstock equation, not those who build the most elegant reactor.

At Sora, we believe the answer has been in the air all along.